As the holidays greet us and this last week meets us with trips to the stores, charges on our credit cards and anxiety that shouldn’t occur during this “most wonderful time of the year,” I’ve decided to re-visit some of the top money mistakes that many of us are making right now.

My desire is that we reset and refocus our finances for the New Year, but it’s not too late to avoid some major money pitfall that might really compound the problem this month if you’re not careful.

Come January, you will be so thankful that you hit “pause” on your finances. These principles matter.

I’ve been sharing our financial journey and frugal lifestyle here on the blog for nearly six years and while we’ve seen significant swings from two parents with no income (season of unemployment), to two parents with dual income, we continually have to re-evaluating our finances.

Finances are such a personal and often times, painful issue.

As I look around me, I’m faced with so many friends that are struggling financially and it’s not just due to a lower income. Many of my friends who are making well above an average income are living paycheck to paycheck.

How does that happen? I’m sure right about now many are wondering the same thing.

Let’s put a stop to these common money mistakes and get more cash in our pockets right now!

Key Money Mistakes:

1. Spending What You Make

Many assume that as long as they don’t spend more than they earn, they are doing well.

That should work, right?

The problem with this mentality is that there is no room for error and it’s the most common money mistake. Spending what you make leaves no room for those “bedlam moments” which arise when you’re least expecting it: the car accident, the water heater breaking, the golf ball shattering the $500 double paned window after you just told your son to stop (not that I’d know any of those from experience, ahem.)

Everyone needs a buffer, an emergency fund, yet if you spend what you make, that portion of your budget never occurs. I wrote about how my car accident reminded me of some important financial principles and this was at the top of that list.

Just recently, I had two different conversations with friends who spent the entire time talking about how tight they were financially. They were behind on bills, paying only the minimum on credit cards and stressed over Christmas purchases. I listened quietly, but realized they were in the midst of implementing this #1 money mistake.

As their paycheck came in, it was going out just as fast (and not on necessities).

One had recently purchased a brand new car and the other was in the midst of major home renovations – any free cash they received went for “wants not needs.” Instead of eliminating financial stress, they traded it for momentary satisfaction only to find it compounded the problem.

So how do we fix this mistake?

Spend LESS Than You Make RIGHT NOW!

That’s the whole premise for gaining financial freedom and no matter what your annual income, baby steps need to be made to achieve this, even if it’s just a small amount.

And yet while it seems elementary, it’s the hardest principle for most to implement because the long slow road is not the one we want to travel. You can do it! Drive the beater car for another year, enjoy the house you have “as is” until you have breathing room, stop buying presents NOW if you can’t pay cash for them and honestly, you will appreciate this season even more. Delayed gratification is where it’s at and you will be so thankful come January.

** As always, I know there are exceptions to this. Please know that medical bills, life changing circumstances etc. are NOT what I am addressing.

2. No Plan for Getting Out of Debt or Creating a Budget

“I’m completely overwhelmed and don’t even know where to start, so I don’t. I just ignore the situation.”

As my friend shared her heart about the credit card debt she’d gotten herself into, I felt the overwhelming burden she carried. Debt is a stifling burden and it affects every aspect of our lives. We tend to rationalize debt and come up with reasons while it’s not “that” bad, but until we are completely free of it, it always looms.

I’ve written a lot about this with many specific suggestions so I won’t offer up any “Stop drinking at Starbucks” as a overly simplistic suggestion to overcome spending problems. Bottom line, we all know that when we are talking about consumer spending issues, the root problem goes much deeper. I agree that small changes in our spending habits equals huge, long lasting savings, I am a walking testimony of that, but for debt issues, a $5 coffee isn’t where it starts.

It starts with a hard core, lifestyle of spending change. You have to be “sick and tired of being sick and tired” of your financial situation and be willing to work hard to make the necessary changes.

You may need to implement tough love in your finances in order to achieve this step. If you struggle with over spending, it may mean cutting up your credit cards and only paying cash. If you feel as if have already cut all your expenses, then brainstorming an additional money stream to raise your income may be necessary. It’s a long road, but it’s SO worth it!

3. Money Secrets

This is a mistake that even the most wealthy make. I continually hear my friends mention, “I know nothing about our finances, my husband takes care of all of that.”

NO!!!! You need to have a handle on your finances, bills, income, debt etc.

Ignorance is NOT bliss!

Whether you are in the midst of financial uncertainty or maybe you just haven’t communicated on the subject of your own family finances for awhile, I encourage everyone to plan a family meeting.

Openly talking about money is often difficult for spouses, yet marriage is a partnership and both parties need to be involved in the process. If you are single, find someone you trust to help you talk through your financial circumstances. The accountability is so helpful.

Statistically, financial problems are stated as the number one reason marriages end in divorce. Marriage is difficult, even when finances aren’t an issue, so add money stress and lack of communication to day to day challenges and slowly the unified front begins to dissolve.

If you aren’t on the same page financially, seek out a Godly financial mentor. I wrote more about this in a two part post, “The Secret Life of Money.”

4. Not Educating Yourself on Major Policies

As the year is coming to a close, many auto policies, homeowners, life and health insurance policies are coming up for renewal. Education is key to fully understanding and getting the most out of these important policies.

We recently bought a $1500 beater, great gas mileage car. Before purchasing it, I called to find out how much the additional coverage would cost us. By the time I got off the phone with my agent, she lowered our overall bill on ALL our vehicles, including this new one by $400/year. She was just as surprised and thrilled that she could find those additional savings. In this situation, I wasn’t calling to negotiate (although I do that on many things), but the relationship, along with her experience, were critical and saved us a ton. It would have never happened had I not made the call.

I asked some Allstate experts for some suggestions on how to better utilize their insurance plans and they were incredibly helpful.

Make sure that you understand what all of the coverages mean. It is not enough to just know that you are covered, but understand what that terms means, and how and when you are insured. With auto insurance, understand how collision coverage might apply even for claims that are not your fault (my friend just found this out TOO late as she found out what was considered chargeable and what was not).

You should talk to your agent any time you have a question. You should also be willing to talk to the agents’ staff, because they are equally knowledgeable and can probably help you as well.

Always discuss claims, as well as review renewals, coverages and price changes. Is your policy for replacement cost coverage or actual cost value? In the event of a claim, will you be able to replace what was lost or will you be paid a depreciated amount?

Of course, let your agent know when you’ll be experiencing a life event – getting married, buying a home, having a baby, etc. – and be open to discussing your Financial policy (Life Insurance), at that time.

5. Overlooking Immediate Ways to Put Cash in your Pocket

While my husband was unemployed, he spent time working alongside our teen boys making $10/hour doing manual labor in the 110 degree NC heat. If you want to create cash bad enough, there are no excuses. Yes, I’m being blunt, but most people just aren’t willing to do whatever it takes. This needs to be a post by itself listing creative ways to create more income. Anything is possible!

Sell something. Yesterday, I put a picture of an old desk I wasn’t using up on FB. It sold. Immediate, cold, hard cash in my pocket. Right now, with a week before Christmas, if you have items you aren’t using, it’s a perfect time to sell them.

Year End Deductibles

These next few weeks are critical for saving the most on end of the year deductions. Read more about Figuring out tax returns here. This can be cash in your pocket.

Luxury Cuts

Yes, these are the most painful. Those steps that most of us don’t want to take, but if you are committed to creating cash flow, they may be necessary. Pair any of these together and $500 can be in your pocket over the next few months.

Cable – a large majority of my readers canceled their premium cable channels, but I was shocked to find how many have completely canceled ALL their cable and have gone to completely online viewing with programming through Hulu, Netflix and others, along with a nice HD antenna.

I haven’t done this yet and honestly, it’s something I really need to think about letting go of (after Hallmark Christmas movie time and football season.) I have had MANY readers give testimonials of how they wouldn’t look back after doing this.

Land line and Cell Phone coverage – if you are still paying for a land line, you are paying for two duplicate services and it will be well worth the effort to check into cutting the land line. Those dollars add up.

Have you looked at your cell coverage lately? Do you need unlimited data? Even with my full time job working online and using my cell phone often, I still have limited data, calls and texting. (And yes, I even saved more when I was on a prepaid phone.)

Call your wireless provider to see what coverage you can eliminate. If you are anywhere near the end of your plan, negotiate. They want your business and they will work to keep you. You’d be surprised at how easy it is. From a parenting perspective, significantly drop your children’s’ wireless plan. When we realized the draw and time temptation that unlimited data had on our first son when he got a cell phone, we immediately slashed it and never looked back.

When I get talking finances, I realize it could be a book, so I’ll stop with these (and continue my list for another post.)

We are all on this journey of learning together. The old cliche, “You can’t live with it, you can’t live without it,” can also pertain to money issues. When we understand its pitfalls and can figure out ways to climb out of them, that’s when the sweet spot begins to occur.

It’s such a blessing to be on the other side and write from experience. I know you will be there soon enough.

I hope this encourages you a bit to pick one thing and just start. It’s all in taking that first baby step towards financial freedom.

What’s your one financial goal for the new year? Maybe voicing it will help you take that step.

Stay tuned for 6-10.

Such great reminders. It’s so easy to get caught up in spending right now.

Great post!

One of my biggest mistakes with money was being disorganized. Not knowing how much $ was coming in and where it was going. Like you said, “Ignorance isn’t bliss.” Tracking it was the best eye opener ever…and telling it where to go (how it was spent), was the best and most powerful thing we ever did.

After this, we both sat down and talked about our financial goals. Once you have goals and talk about them together, it’s amazing what you can accomplish. We’re at $85K paid off in debt since January 2013 and going strong!

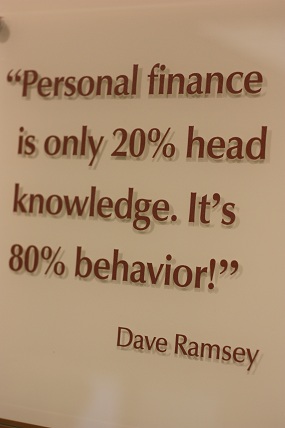

Was listening to Dave Ramsey recently and he said something truly powerful! Something to the effect of your goals should be more important than your everyday desires!

My goal is to figure out how to communicate on finances with a spouse that is working for no paycheck. I am a stay-at-home-mother ( =$0 “take-home”) and, after 27 years with the family business, my hubby offered to take no pay! And he does not like to talk about money at all. Marriage 101 here we come!